![]()

Today, Madrona announced the 5th annual ranking of the top 40 private AI companies — the 2025 Intelligent Applications 40. The 2025 winners feature 27 new companies compared to last year, which is an unprecedented 68% turnover in annual winners, highlighting the broadening innovation in applied AI.

Databricks is the only company to have made the list all five years. Combined, these 40 companies have raised almost $120 billion in capital to date.

To create this year’s list, more than 70 venture investors across 54 leading venture and corporate investment firms nominated and voted for 340 companies. In partnership with PitchBook, we integrated data-driven scoring into the evaluation process, adding rigor and depth to the final results.

Many of these companies will be featured at the 4th annual IA Summit, taking place on September 30th and October 1st in Seattle, hosted in partnership with AWS Startups, Microsoft, Google Cloud, McKinsey & Company, NYSE, Goldman Sachs, and Delta. You can find out more on the event site and request an invite.

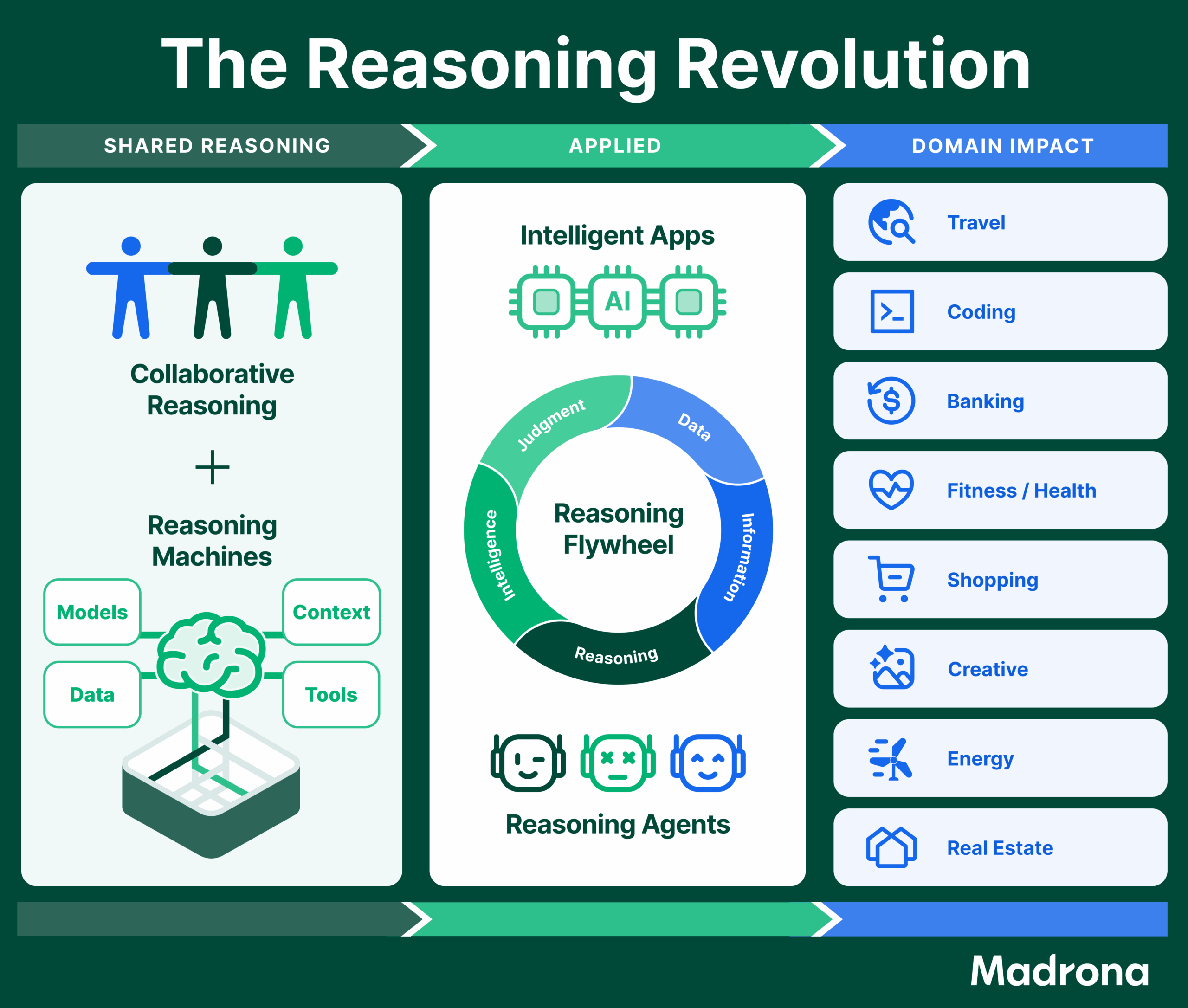

There have been critical AI breakthroughs over the last twelve months since we announced the 2024 IA40 cohort. The market has seen renewed IPO activity (including Figma’s recent IPO), blockbuster acquisitions like Wiz’s sale to Google, and record-setting fundraises. AI systems and processes are gaining adoption in even the largest and most intentional enterprises, and emerging innovations are poised to transform the nature of work across entire industries. We have framed this transformation as the Reasoning Revolution, which will be the overarching theme of the 2025 Summit.

Anthropic’s launch of MCP in late 2024 introduced a reliable and structured interface layer for connecting AI models with tools and data, fundamentally shifting AI from model-centric assistants to intelligent applications and agents. The AI agent infrastructure stack continues to evolve with companies being built across tools, data, and orchestration layers at a breakneck clip. At the application layer, there has been an explosion of CodeGen tools reshaping software engineering, including Cursor, which powers nearly one billion lines of code generated daily and is valued as a company at nearly $10B. Google and Microsoft recently claimed that 30% of their code is now AI-generated.

As we reflect on our fifth year of recognizing the top global private AI companies, we see momentum continuing to build in Applied AI since the initial list was released in 2021. The field of both intelligent applications and enabling companies remains highly dynamic, with the 2025 IA40 list featuring only 13 repeat winners. This is fewer than what we observed in 2024, which is no surprise, as companies are achieving momentum and capturing value at an unprecedented pace. Many outstanding companies just missed making this year’s group. Previously, only four companies — Abnormal, Databricks, Hugging Face, and Runway — had appeared on the IA40 every year from 2021 to 2024, but only Databricks made the list as a five-time IA40 winner.

At the 2024 IA Summit, we observed several key themes, including the unabated pace of AI funding. OpenAI had announced the largest venture funding round ever at that time of $6.6B, a feat that was then quickly overcome by Databricks raising a $10B round at the end of 2024 (and a rumored additional round coming soon). OpenAI’s latest raise outpaced both those rounds by raising $40B at a $300B valuation, the largest private tech deal on record, increasing the prospects for the first AI-native, trillion-dollar company.

Meanwhile, beyond the giants, new enablers and intelligent applications continue to diversify in the disruptive value they provide, as models are not all you need. Infrastructure and applications continue to evolve in tandem as intelligent applications achieve buy-in from new verticals and, in turn, create demand for more sophisticated infrastructure, as evidenced by the industry categories on the list that continue to evolve. Competition among enablers is driving both scalable and affordable infrastructure, while competition among applications is forcing innovation in agentic capabilities and value delivery. Vertical applications are increasingly gaining momentum as they find alignment across domain expertise, workflow depth, and measurable ROI. The bar for what defines a top 40 private intelligent application company has never been higher.

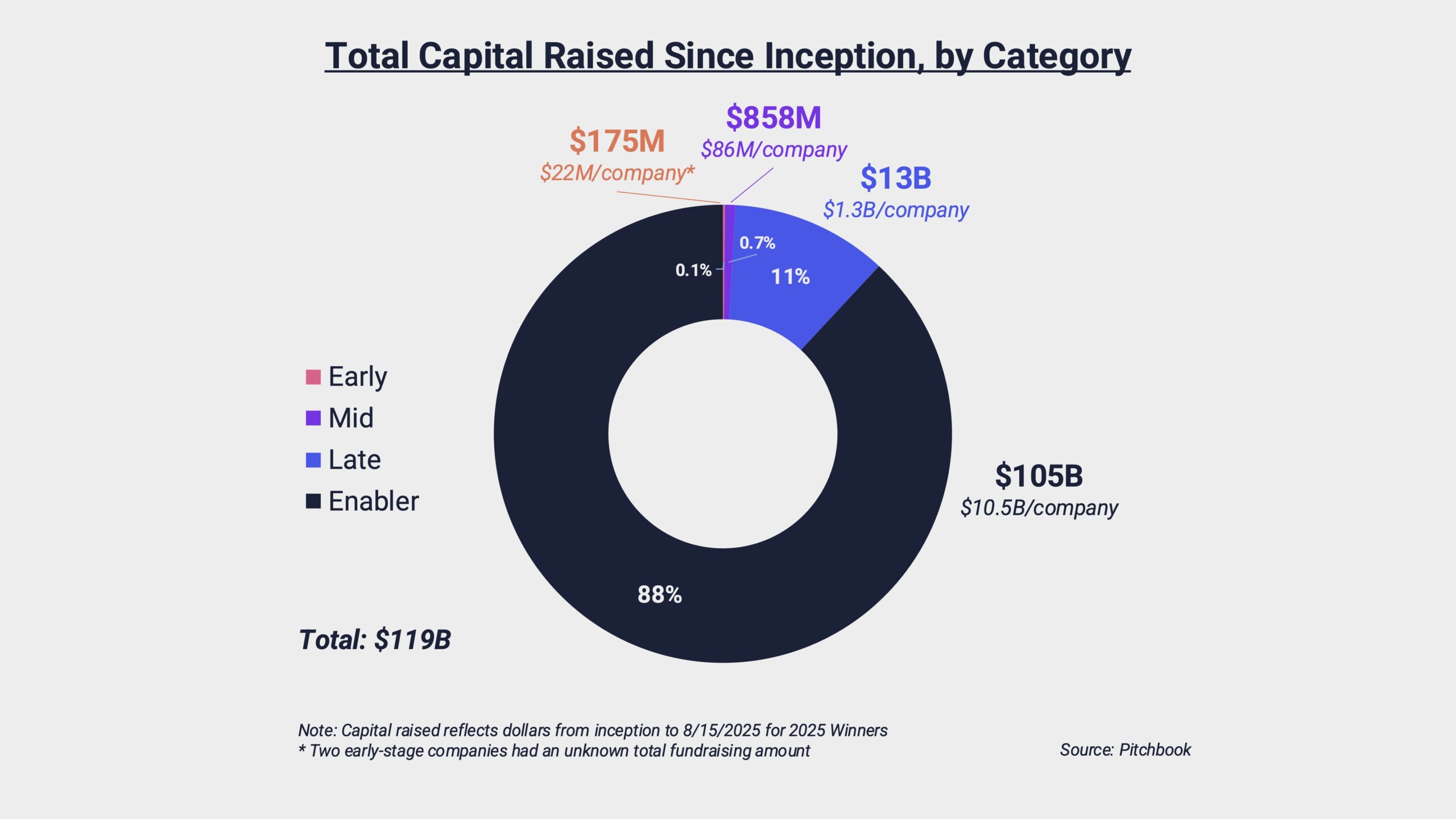

The 2025 IA40 winners have raised a total of $119B from inception to August 15, 2025 (the cut-off for tabulation). Over 70% of the total, or $86B, was raised in the last 12 months alone, another data point for accelerating AI funding. The funding is also highly concentrated. More than 85% of the total, or $102B, was raised by just three companies (OpenAI, Anthropic, and Databricks). The remaining $16B was raised by the other 2025 IA40 winners. Of course, that still means that, on average, each of the other winners has raised $432 million to date.

The concentration in capital aligns with an analysis of 18 top AI native applications with over $50M in annualized revenue, which revealed that OpenAI and Anthropic capture 88% of the $18.5B cumulatively generated revenue.

Fundraising remains strong for prior IA40 cohorts as well. The 2024 IA40 winners raised $92B over the last 12 months. This figure is double that of all funds raised by these winners from inception to August 2024, or $45B, reflecting the scale of investment acceleration. The 2024 winners included two major IPOs, Figma and CoreWeave, which disqualified them from making the 2025 list, but signal the growing public market appetite for AI-related companies. There were also a couple of notable acquisition exits among this cohort. Google acquired Wiz for $32B, and Nvidia acquired CentML, rumored at $400M. We continue to observe the power of strong balance sheets of the tech hyperscalers and their growing interest in fast-scaling, maturing AI-native companies.

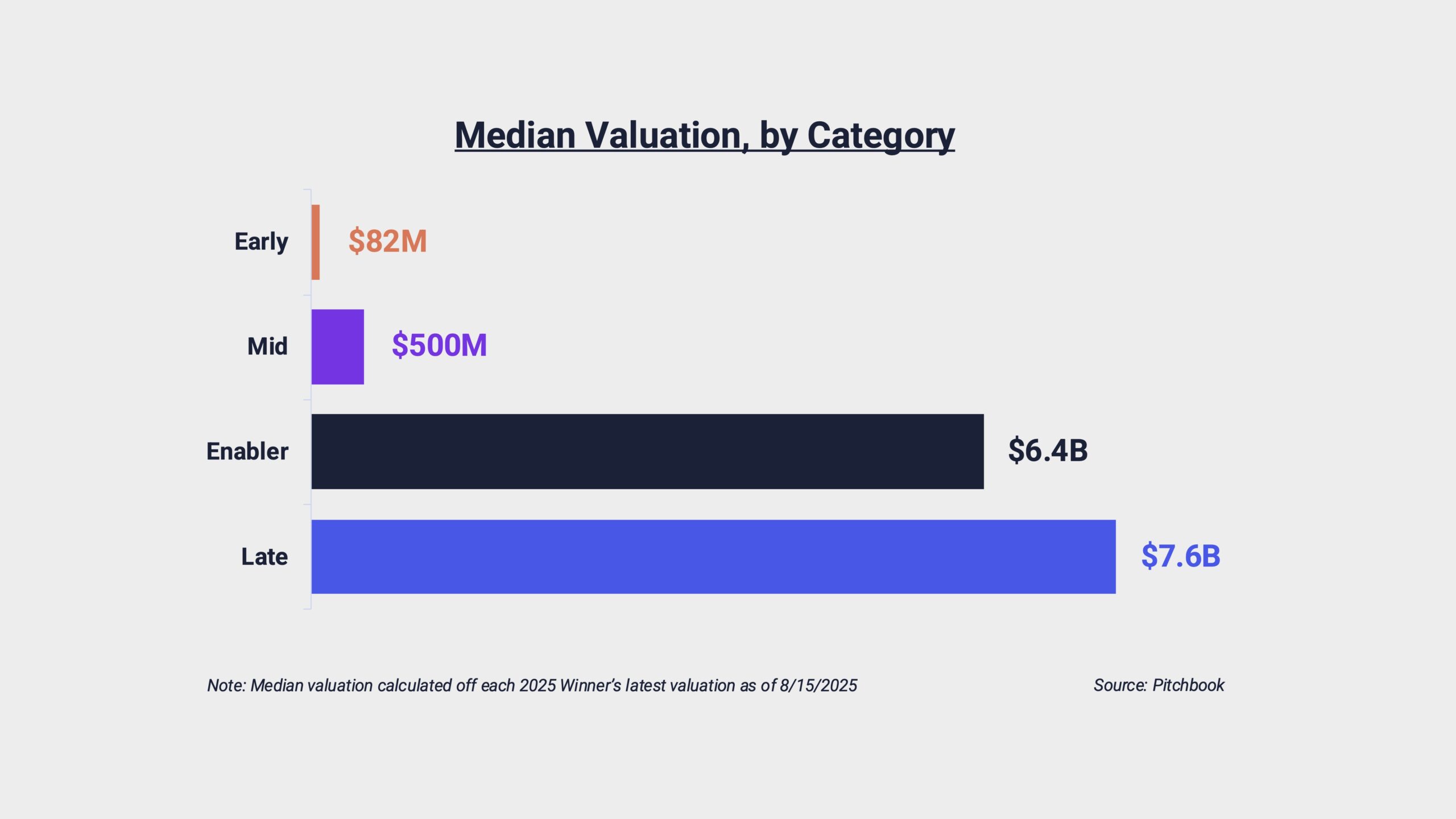

The IA40 companies are split across four categories

- Early – Up to $30M total capital raised

- Mid – $30M – $200M total capital raised

- Late – $200M+ total capital raised

- Enabler – Stage Agnostic (We define enablers as the companies building the tools and infrastructure that enable intelligent applications.)

Funding data categorized as of 8/15/2025

This year, we continued to feature five Emerging Enabler Winners. These five companies represent enablers that have raised less than $50M of capital and were top runners-up for the list.

Key Takeaways From the 2025 IA40

New user interfaces for AI are taking off as AI becomes increasingly adaptive, agentic, and conversational across modalities.

User interfaces are shifting from static menus to multi-modal context-aware experiences. Natural language, whether spoken or typed, is quickly becoming the default way people interact with software, replacing rigid navigation with fluid, intent-driven interactions. Companies like HeyGen are showing how video avatars can create more natural, human-like front-end user interfaces, while Cartesia and ElevenLabs are pushing boundaries in voice and audio interfaces that respond dynamically in real time. OpenAI’s Agent, Perplexity’s Comet, and Vercept’s Vy all highlight the move toward agentic interfaces that span the browser and adapt fluidly to different contexts, enabling AI to execute tasks, gather information, and orchestrate workflows with minimal effort from users. As interactions increasingly flow across text, voice, image, and video, demand will continue to accelerate for AI experiences that function less like tools and more like adaptive copilots across every surface.

Market opportunity sizes and demand in the age of AI are large enough to support multiple scaled winners, including coding and “vibecoding.”

At the 2024 IA Summit, a key takeaway was that the killer use cases are starting to emerge. And nowhere is that more apparent today than with AI companies in software development. A transformative $750 billion opportunity is developing, driven by AI tools that are reshaping the entire development lifecycle. Tools such as Cursor, Vercel, Lovable, Bolt.new, and Factory enable natural language–driven coding, debugging, and deployment, turning what once took weeks into tasks even a non-developer can deliver in minutes. Rather than simply lowering costs, GenAI is merging the long-separated IT services and software tools budgets, allowing AI-driven platforms to replace traditional, labor-intensive IT engagements. Startups that provide seamless, high-leverage entry points that can scale into full developer workflows are positioned to become winners in enterprise software development.

AI companies are experimenting with and seeing success with new business models that are more value-aligned with their customers.

The shift underway from SaaS subscription-driven approaches is not just about embedding AI into existing workflows, but also about redefining the very business model of software. Instead of selling tools with static features, companies are beginning to prove the success of selling services powered by software — where outcomes, not the tool, become the product. This “service-as-software” model blurs the line between SaaS and IT services, as AI employees handle work that once required human effort. Compelling examples are emerging across domains, from companies like Distyl AI developing and deploying scalable AI solutions for enterprises, to companies like Aaru that are fundamentally disrupting the nature of market research with simulated users where monetization no longer scales as pay-per-complete. We expect to see more winners successfully unlock new pricing, engagement, and value-capture mechanisms (like hybrid consumption and subscription models and new units of consumption measures) to fundamentally reshape how AI value is quantified and captured.

Thematic Insights: AI Applications

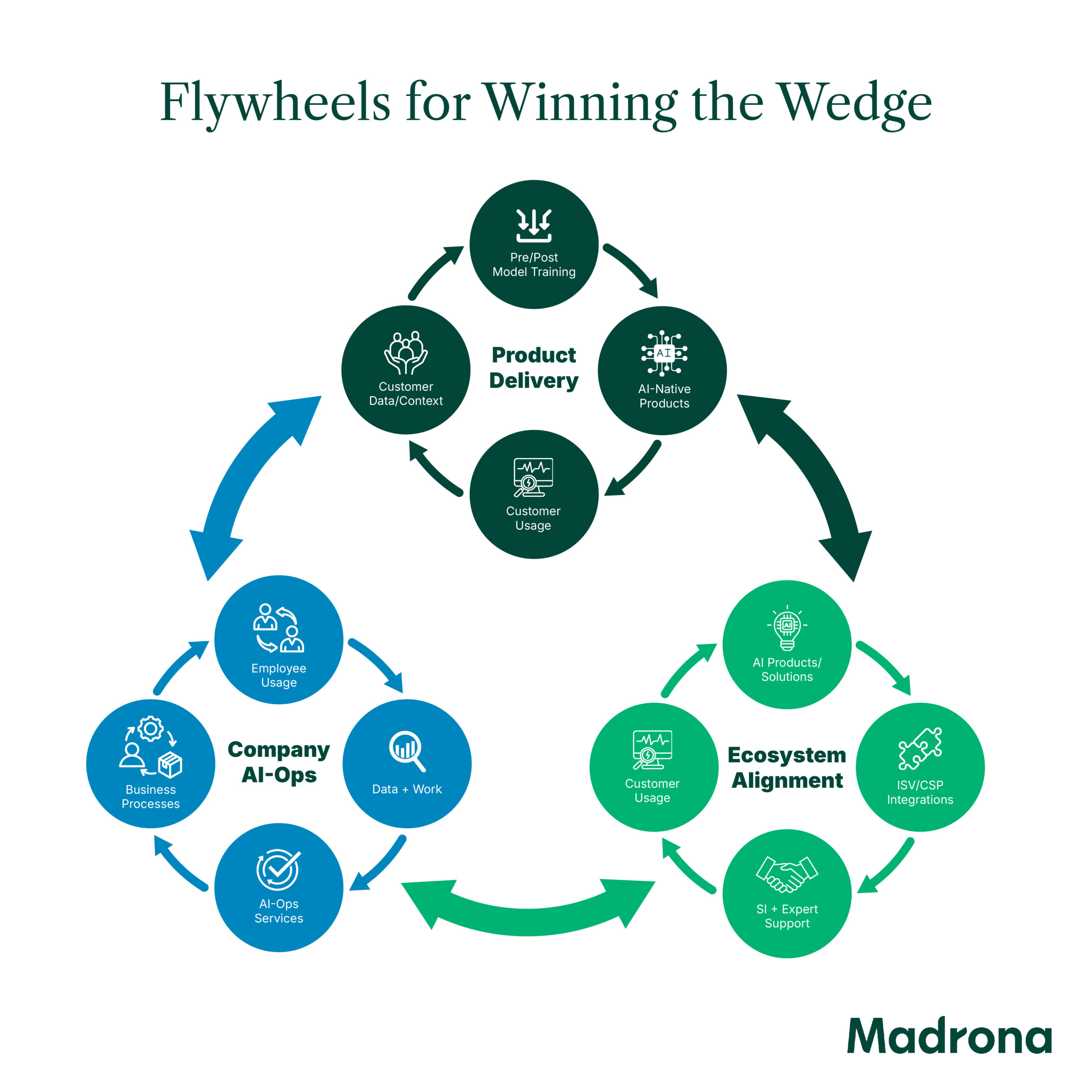

Competition at the application layer continues to heat up. AI leaders in certain verticals and functions that are breaking out have cracked the flywheels for winning the wedge.

The rise of AI-native companies is not just about rapid product launches and early customer traction, but also about learning how to turn that momentum into durable advantage. Winning an initial customer wedge is only the beginning. Enduring companies compound their edge through three key reinforcing flywheels: product delivery, company operations, and ecosystem alignment flywheels. Companies such as Legora for legal, CodeRabbit for code review, and Gamma for content creation are executing well along the product flywheel, where their products continually improve with data and usage, creating a self-reinforcing and improving loop of value. Companies such as Abridge and Anduril have unlocked the ecosystem flywheel, with Abridge partnering with organizations across healthcare systems, EHR vendors, and payers, and Anduril partnering with both big tech and military strategics. The company operations flywheel is less externally apparent, but just as critical. These flywheels in motion build defensibility that speed alone cannot provide. And we believe the companies that master all three will continue to define the next generation of enduring AI application leaders.

Intelligent application companies are moving beyond solely serving enterprises and prosumers to address the needs of consumers.

Just as software development is evolving from code generation to vibe coding, we are seeing a similar “Vibe-X’ing” trend across verticals from tools designed for professional users to ones that encompass general consumers. In the software vertical, as Cursor has scaled, we have also seen rapid adoption of tools such as Lovable, Bolt.new, and Vercel’s v0. We are beginning to see this trend scale in other verticals such as content creation, with even AI-enhanced companies such as Canva and Figma moving towards this trend. The evolution around “Vibe-X’ing” is also reflective of the evolving user interfaces mentioned earlier with natural language as the new modality for action, which democratizes skilled creation to a much broader base of users. These new applications also have the potential to fundamentally shift hiring and enable lean teams to go big.

Thematic Insights: Enablers

The data layer is a fundamental enabler of AI reasoning and automation, powering the contextual fabric that allows applications to scale from tackling narrow tasks to enterprise-wide decisions.

The fact that Databricks has remained a five-time winner of the IA40 list reflects the importance of the modern data layer as a foundation of the AI stack, unifying the data and analytics to make applications effective. Without reliable, accessible, and continually refreshed data, even the most sophisticated agents cannot reason, adapt, or improve over time. The shift that Databricks made in developing its lakehouse architecture has enabled AI agents to access both structured and unstructured data at scale, while also enabling the data flywheel through continuous ingestion, annotation, and retrieval. Databricks is also highly complementary with others that touch the data layer, including Clickhouse, which has been a transformative leader in real-time analytics for powering user-facing applications. These data and analytics infrastructure players will continue to play a steadfast role with AI. And we wouldn’t be surprised if Databricks makes it again in 2026 as a winner (unless they IPO).

The AI-native agentic infrastructure stack is more streamlined and interconnected than ever before.

Protocols such as MCP and A2A have redefined the foundations of agentic applications and are spurring a feedback loop of demand between applications and the underlying infrastructure. Application companies are leaning into this shift: Exa has a popular MCP server that allows AI assistants to perform real-time searches to retrieve structured web results leveraging Exa’s API. On the infrastructure side, Browserbase is extending agent reach into data-rich services and the browser, while others, such as Statsig, are enabling AI clients to interact with their API, accelerating exploration of experiments, feature flags, and analytics. This growing ecosystem reveals a two-sided dynamic. One side where demand is driven by innovative developer tools, and the other where an expanding supply of MCP servers unlocks entirely new capabilities, letting agents connect to services, data sources, and business logic without bespoke wiring. Beyond MCP, agents are now orchestrating across tools, data, layers, and workflows, enabled by innovations in orchestration frameworks such as Langchain and CrewAI. These new protocols and frameworks will enable and unlock new agentic reasoning, memory-sharing, and execution across domains.

Looking Ahead

We are entering an era of innovation driven by reasoning machines, or intelligent systems that go beyond curated data and models to enable true collaboration between humans and AI. Across industries, reasoning agents are beginning to reshape how decisions are made (spanning planning, discovery, strategy, and execution), creating reasoning flywheels that appreciate in value over time. As this Reasoning Revolution unfolds, these AI-powered systems promise to amplify human capabilities more profoundly than any prior technological leap.

With a warming IPO market and hyperscalers on a competitive hunt for both strong AI companies and talent, we anticipate more IA40 winners to exit over the next year. We also expect to see continued high turnover in next year’s list, driven by maturing companies across promising themes. This includes companies optimizing content and insights for brands in the next generation of search, as well as companies scaling both the infrastructure and user interfaces of agentic commerce.

For more than a decade, Madrona has worked alongside visionary teams building intelligent applications, helping them transform industries and redefine what software can achieve. The IA40 companies are shaping the next era of how humans interact with technology, and their breakthroughs merit recognition and celebration.

You can read more about the process and methodology here.

The 2025 IA40

Early

1 Distyl

2 Listen Labs

3 Exa

4 CodeRabbit

5 Gamma

6 Fireflies.ai

7 Pylon

8 Factory

9 Clarify

10 Aaru

Mid

1 Granola

2 Linear

3 Mercor

4 Cartesia

5 Basis

6 Prophet Security

7 HeyGen

8 Legora

9 Bolt.new (StackBlitz)

10 Dropzone AI

Late

1 Lovable

2 Cursor (Anysphere)

3 Anduril

4 Abridge

5 ElevenLabs

6 Perplexity

7 Canva

8 Applied Intuition

9 Clay

10 OpenEvidence

Enabler

1 Anthropic

2 OpenAI

3 Databricks

4 ClickHouse

5 Vercel

6 Together AI

7 CrewAI

8 Fal

9 Browserbase

10 Statsig

Emerging Enabler

Modal Labs

Haize Labs

Braintrust

Langchain

Arcee.ai