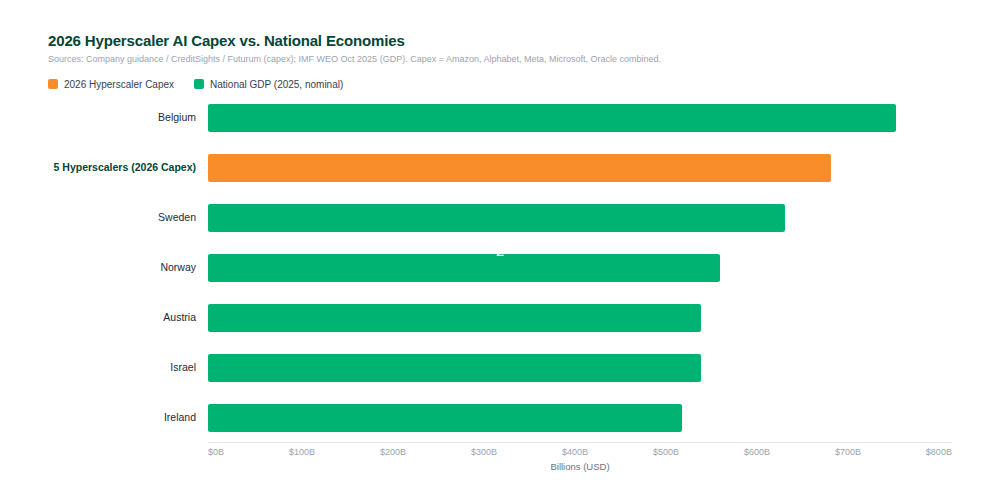

Much ink has been spilled about the concentration of capital at the AI infrastructure layer: hyperscalers on pace to spend $650-700B in 2026 alone, foundation model companies valued at the GDP of mid-sized European nations, a buildout that by the end of the decade will likely total $5-7 trillion. But many early founders are wondering about the implications for their fledgling companies. Here we want to answer that question head on.

That lofty concentration of capital at the model and infrastructure layer is simultaneously uncovering the ground on which the most interesting company-building opportunity in a generation is sitting, if you build in the right places.

The model is becoming infrastructure

Frontier models are extraordinary. They can reason, write production code, parse complex documents, and navigate domain-specific workflows that once required years of specialized training to perform. But the competitive gap between the leading models is narrowing fast. Benchmark leadership rotates every few months. Prices are collapsing: Anthropic cut API pricing 67% in a single move, Google followed. The raw intelligence layer is being commoditized at nation-state expense, and that process will continue as the buildout scales.

This is the founding condition of the current opportunity. When a powerful capability becomes infrastructure, the value shifts to whoever builds the most useful and defensible systems on top of it. It happened with cloud computing. AWS made compute abundant and cheap, and an entire generation of software companies was built on that foundation, not competing with AWS, but made possible by it. The same dynamic is playing out now, faster and across a broader surface area.

Our colleagues Sabrina Albert and Vivek Ramaswami wrote recently about why frontier models will expand the opportunity for startups rather than foreclose it, and about the agent harness concept specifically: the system wrapped around a model that turns raw capability into reliable outcomes. It’s worth reading alongside this piece. What we want to add is something more specific: not just that the opportunity exists, but where it is concentrated and why certain positions will prove durable while others won’t.

Where foundation models won’t go

Foundation model companies are moving fast and moving vertical. That’s real and founders should take it seriously. But there are structural limits on where they can or will compete, and those limits define the most defensible positions available to startups right now.

The first limit is liability. Foundation model companies are general-purpose platforms. They are not going to absorb the legal, regulatory, and financial accountability that comes with owning specific outcomes in specific industries. A platform that files your taxes across 40 jurisdictions and faces audits on your behalf is not a product Anthropic is building. A system that owns the compliance trail for a healthcare provider, or underwrites insurance risk, or manages audit-ready accounting for an SMB: these require not just technical capability but institutional accountability. That accountability is a moat. Every audit successfully navigated, every jurisdiction mastered, every edge case handled adds to a body of institutional knowledge and credibility that compounds in ways raw intelligence cannot replicate.

The second limit is proprietary data. Foundation models are trained on what exists publicly. The data that lives inside a specific industry’s workflows — clinical notes, proprietary financial models, construction project histories, legal matter files — doesn’t. The startups that embed deeply enough to generate and accumulate that data, and build systems that improve as that data compounds, are building something the model layer genuinely cannot commoditize. The data isn’t just a training asset. It is the product becoming more valuable with every customer interaction.

The third limit is workflow complexity. There is a category of problem that cannot be solved by throwing more intelligence at it. Cross-border regulatory coordination, multi-party transaction workflows, clinical decision support embedded in existing care pathways: these require deep integration with messy, real-world systems that have been built over decades and don’t move because a better model became available. A startup that spends two years embedding into how a construction firm actually manages change orders and lien waivers has built something that a foundation model company, however well-resourced, has no particular incentive to replicate.

How to build for durability

The harness concept is the right mental model for how to build. The model is the engine. The harness (the orchestration layer, the evaluation loops, the tool integrations, the guardrails, the memory systems) is what turns that engine into a product that reliably delivers outcomes. Startups that compete on model capability are building on sand. Startups that build harnesses designed for a specific workflow, embedded in a specific industry’s data and accountability structures, are building something that compounds.

The distinction that matters most is between tools and outcomes. A tool for lawyers is a different business than a platform that owns the malpractice exposure. A coding assistant is a different business than a system that owns the deployment pipeline and the audit trail. Tax calculation software is a different business than a service that files, faces audits, and guarantees accuracy. In each case the second position is harder to build, harder to displace, and harder for a foundation model company to absorb. The accountability that sounds like risk is actually leverage.

The practical implication: when evaluating where to build, the right question is not whether the problem requires intelligence. Everything will soon. The question is whether the solution requires something more than intelligence. Regulatory relationships. Institutional trust. Proprietary data loops. Real-world accountability. Those are the ingredients of durability in an era where intelligence itself is becoming abundant.

The window is open, but it won’t stay that way

The cost of entering a vertical has never been lower. Frontier model APIs give a small team the domain scaffolding that incumbents spent a decade building. The engineering bottleneck that historically limited vertical software to two or three serious competitors per market is gone. A founder with domain expertise and a clear customer can move faster and go deeper than was possible at any prior point in the history of software.

But the same forces that lower barriers for startups are accelerating the pace at which foundation model companies and large horizontal platforms push into vertical territory. The wedge a startup chooses needs enough real-world complexity to survive long enough to expand into a defensible position. Thin wrappers around foundation models will not hold. Products that compete on interface or convenience will get absorbed. The window to build something durable is open, and it favors founders who move with urgency toward the hardest, messiest, most accountable problems in the sectors they know best.

The infrastructure being built right now is a bet that AI will transform every industry. For founders, the question is which part of that transformation requires something that money alone cannot build.