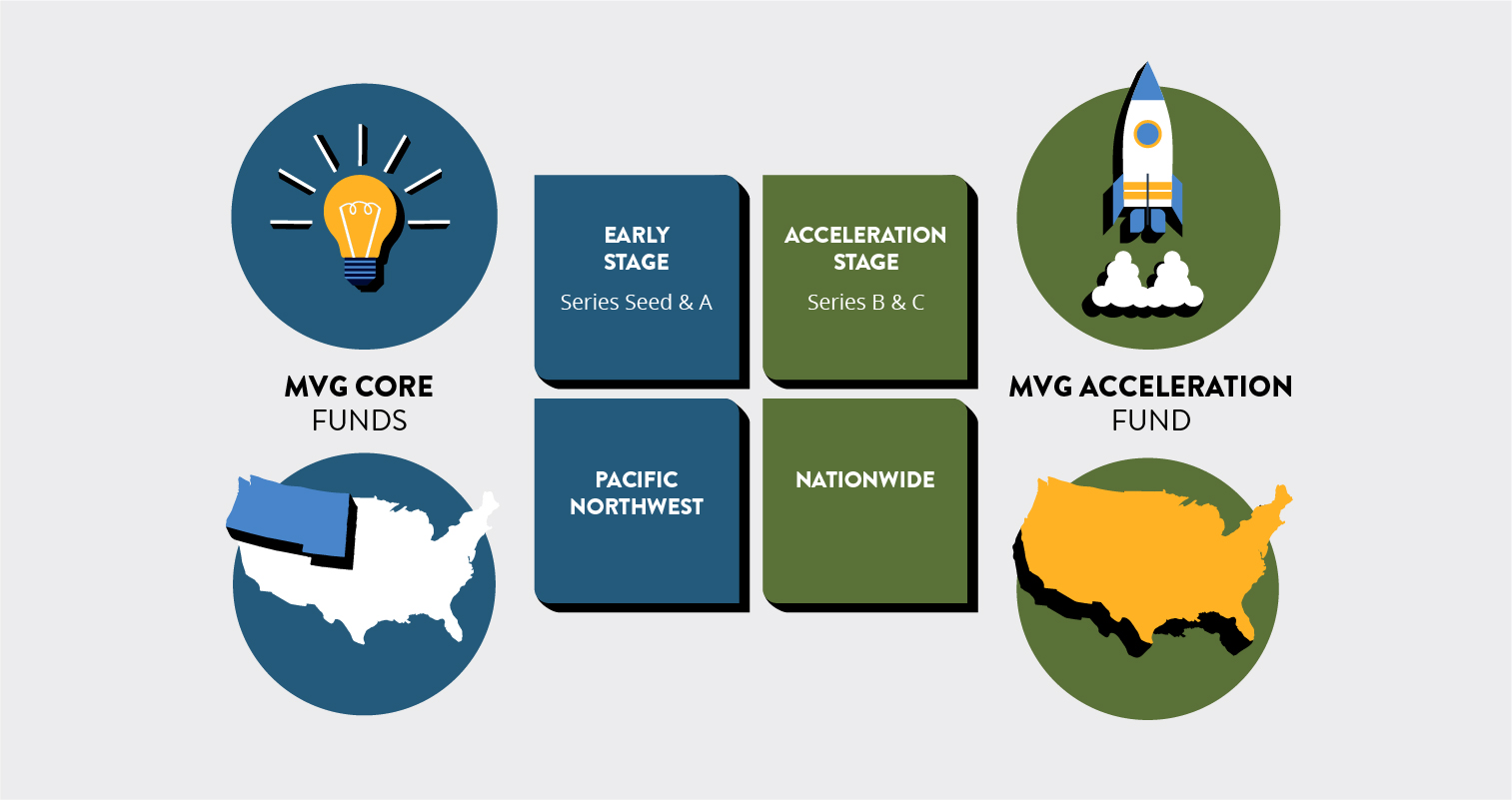

Today we are introducing a new Madrona fund, the $100 million Madrona Acceleration Fund. This new fund expands our ability to work with entrepreneurs around the country as their companies move from product-market fit to accelerating business growth.

Over nearly 25 years, Madrona’s main passion has been working with exceptional entrepreneurs from the earliest stages by rolling up our sleeves to help them build successful companies. We believe that getting involved at an early stage (seed and Series A) is primarily a local business. Our focus has been on the Seattle/Pacific Northwest region which is one of the leading centers of innovation in the world. It can take more than a decade to build a great and lasting company and we have been there for all the ups and downs of the journey. Amazon, Apptio, Isilon, Impinj, Redfin and Smartsheet are just some examples of Madrona’s strategy in action.

As other companies find product-market fit, we believe there are investment opportunities where Madrona can add value in a complimentary way to existing investors and help this additional set of companies succeed. So, today we are announcing our first $100 million Acceleration Fund to make initial Madrona investments at a Series B or C stage in leading companies in both the Pacific Northwest and beyond. For us, Acceleration Stage means the company has strong evidence of product-market fit, has demonstrated customer value and product differentiation, and has complimented exceptional founders with key executives to help build AND sell those products. Additionally, we look for market signals that indicate the company has a clear path to become a lasting and significant company. With this new fund, we will lead rounds or partner with other investors on a few select Acceleration Stage companies each year.

MADRONA VENTURE GROUP FUND STRATEGY

Some folks have asked us why we are creating the Acceleration Fund and why now? We wanted to share with the innovation ecosystem, and especially entrepreneurs, how we are thinking about this opportunity:

- Madrona has nearly 25 years of experience and success adding value at every stage of a company journey – from Day One for the long run. This includes the acceleration stage of growth that is often marked with a B or C funding round, and then the ongoing progress that lead to IPO’s or M&A outcomes.

- Our hometown, greater Seattle, has emerged as a global leader in cloud computing, AI/ML, new retail and much more. Madrona has been an early leader and investor in these sectors leveraging our longstanding relationships with outstanding research organizations like the Paul Allen School of Computer Science at the University of Washington and Allen Institute for Artificial Intelligence and outstanding entrepreneurs.

- Seattle is home to two of the top three largest market cap companies in the world (Microsoft, Amazon) and a thriving ecosystem. Madrona has a proven ability to help companies navigate and partner with these companies as well as the over 100 global technology companies that have a significant presence in our region.

- We have built deep relationships with entrepreneurs, co-investors and strategic partners who increasingly encourage us to evaluate new Madrona investments at the acceleration stage (examples include Accolade, Jama, Snowflake, Tigera, and UIPath) in our region and beyond it.

- Being self-aware, we have also missed out on investing in some high potential, Seattle area acceleration stage companies. Quality companies like Outreach, iCertis, Textio and Auth0 come to mind. We are excited to be considered by both best-in-class acceleration stage companies around the country and in Pacific NW companies where management teams believe we can add complimentary value for their next stages of growth.

We believe our understanding of building value from an acceleration stage forward is differentiated and high impact. But, the real validation comes from what entrepreneurs believe and the results their companies produce.

Mark Mader, CEO of Smartsheet

“Madrona invested in Smartsheet in the Series A and then two years later during the depth of the recession with a product revamp in front of us – they invested further. As product-market fit was achieved and we scaled 20x, they also effectively partnered with other investors — all the way through to our IPO in 2018. Madrona delivered value across hiring, partnering, go to market strategy, capital raising, and more. High quality companies poised for growth will clearly benefit from the new Acceleration Fund.”

Daniel Dines, founder and CEO of UIPath

“UiPath has been on a long journey of growth and when we first started talking about building an R&D center in the Seattle area, I immediately knew we needed a local partner with experience building products, teams and go to market partnerships. We found that in Madrona. The team has helped us accelerate some key product strategy objectives, recruit important team members to help scale the team and also connect with local technology and business leaders at Microsoft who are very important to fulfill on our partnership goals together.”

Raj Singh, CEO of Accolade

“When I joined Accolade almost four years ago – the mission was to accelerate the company’s growth by finding the best talent to build a world class product and distribution team. To do that, you need world class partners. Having worked with Matt McIlwain and Madrona on both the Apptio and Amperity board of directors, reaching out to Madrona was high on my priority list on day one. And they have lived up to my expectations – helping with customer acquisition, critical hires, key partnerships, and invaluable counsel.”

Let’s talk!

Madrona has been adding to our team so that we can continue to partner with our Day One investments over the long term and selectively make a few acceleration stage investments each year. Hope Cochran, with over two decades of scaling, taking public and guiding exceptional companies, recently became a Managing Director. Sudip Chakrabarti, with extensive experience investing in Silicon Valley, moved up last year to join us as a Partner. Katie Drucker became our Head of Business Development and Partnerships. And, we continue to add to our network of Venture Partners and Strategic Directors with a set of highly accomplished leaders including Terry Myerson, Luis Ceze, Betsy Sutter, Ted Kummert and Mark Britton.

We look forward to investing with companies that are approaching the “acceleration stage” of their company life and are interested in exploring a fit with Madrona. We are looking to lead rounds, partner with your existing investors and roll up our sleeves as a team to have a positive impact on your company’s trajectory. So, please reach out to one of us directly or feel free to send a note to [email protected].

There has never been a better time to be an entrepreneur and innovator. And, we believe, it is essential to have the “Seattle Perspective” as part of your team to accelerate growth and maximize long-term value. We encourage you to talk to the entrepreneurs, co-investors and partners we have had the honor to work with for almost 25 years. And, we look forward to being a resource to you in the months ahead.